Lesson 1: Creating a wealth practice

Learning Objective

Creating a wealth practice – finding the balance for what works for us and that aligns with our personal values and circumstances

Many of us tend to think that getting ahead with our finances is excessively complicated. But in reality, it’s more important to learn the simple skills and manage our behaviour than it is about mastering complex investing techniques.

I often say, in order to manage money well, we need to manage our selves well and this is the key theme for this week.

All the technical skills we need for our wealth practice can be learned – it is not rocket science. It’s about common sense and finding the balance for what works for us and aligns with our personal values and circumstances.

Investing is about growing and nurturing savings to create more wealth for the future – to find ways to invest that we are comfortable with – to provide a reasonable return for any risk that we take. We must understand the implications of using borrowed money to grow our wealth for the future. We also need to protect ourselves, after all, life happens – there are ways that we can protect our families; our future; our financial wellbeing and ourselves. It may include having a cash buffer, protecting our income or insuring our assets or debts in the event we become sick, suffer an accident or can’t work.

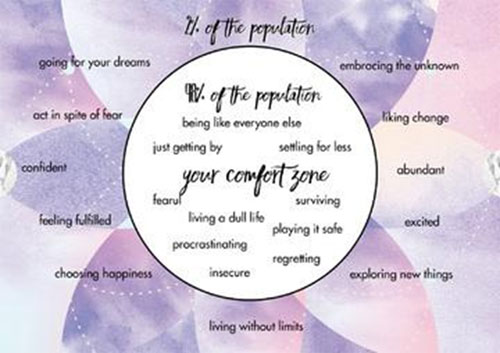

Comfort Zone

Albert Einstein famously said “The definition of insanity is repeating the same behaviours and expecting a different outcome” and this saying rings true for a wealth practice.

We can’t keep doing the same things, living in hope that something will change and we will magically be wealthier. We need to take action and make changes – to step outside of our comfort zone – to expand and create new opportunities, grow and create a new wealth practice.

For us to change and attract more in our life

we need to be open and willing

– to feel comfort in discomfort –

that is where the growth is; where the gold is.

The function of our sub-conscious mind is to store and retrieve data and ensure that we respond the way we have been programmed to. This keeps us thinking and acting in a consistent manner and in alignment with what we’ve always done and said in the past.

This effectively creates a comfort zone, which is why we often find it difficult or uncomfortable when we do something new or different, or try to change our already established patterns of behaviour.

Our brains resist change so when we’re doing things we haven’t done before, our brains send an alert to us, this isn’t normal and we shouldn’t be doing this.

Our comfort zone also creates a false sense of security, stay here, it is safe and you are protected.

But staying where we are is doing more harm than good. Our comfort zone is an illusion. It often feels comfortable, but makes us feel stuck; we need to step out and make the changes to live a wealthier abundant life.

Often we become so used to living in our current comfort zone that we begin to cling to it – when better opportunities come up, we tend to pass them up because we aren’t brave enough to step outside and change.

Even if we are unhappy and want to change our lives, often we resist what it takes to step out of our comfort zone to a wealthier, happier life because it is too hard – we are stuck and we keep doing what we’ve always done, safely – nothing.

The thing is, our future possibilities arise only when we have the courage and determination to step outside the comfort zone. We resist investing because it feels too risky, we ruminate on questions, such as; How do we know what to invest in? Who can we trust? What happens if we lose all our money?

Today I release old habits to make space for new, more positive ones.

And, while it may feel good sitting in our security, not investing – doing nothing can mean we lose out in the long-term – missed opportunities, missed wealth.

“Come to the edge,’ he said.

‘We can’t, we’re afraid!’ they responded.

‘Come to the edge,’ he said.

‘We can’t, we will fall!’ they responded.

‘Come to the edge,’ he said.

And so they came.

And he pushed them.

AND THEY FLEW.”

-Guillaume Apollinaire

Financial Independence/ Financial Freedom

Creating a wealth practice helps us to create financial freedom, independence. When most of us think of financial independence or freedom, we refer to retirement and we often think that retirement is something that only happens in our 60s or 70s. But financial freedom and independence, even retirement can happen when we have enough financial resources to support ourselves and meet our needs and wants without the need to necessarily work – or work as we know it – work becomes a choice.

Financial independence gives us choice to live the way we want to, to pursue things like travel; a new career; a passion; a volunteer or spend more time with family.

Financial Freedom is a term that is used, and misused a lot.

One definition is: when we are in control of our finances, we are able to choose what to do, when we want to do it.

Mindful question/reflection: How do you define financial freedom?

Have you only thought of retirement in your 60s or 70s?

At what age would you like to be financially independent or free?

Mindful Exercise:

Imagine for a moment, we have $40,000 in an account and so does our friend Sarah.

We are both the same age.

We both have the same amount of money contributed by our employers on our behalf.

Both accounts are invested the same way; we get the same return each year on our money.

The only difference is we are paying 2% pa in fees, and Sarah is paying 1% pa in fees.

The 1% pa difference in fees each year means that Sarah will have 20% more in her super than us in 20 years’ time.

Fees really do matter.

Now, imagine that we both have $40,000 in superannuation.

Again, we are both the same age.

We both have the same contributions by our employers on our behalf. This time we both pay the same fees of 1% pa, but this time, we have decided to invest our balance in a different investment option. Although the investment options are the same cost, their performance is different.

Each year, Sarah’s investment option performs 1% better than ours does and this 1% difference in performance each year will also mean that Sarah’s going to have a lot more than us in 20 years time.

Performance also matters.

Did you know? The Australian Taxation Office reports there is over $14 billion in lost super waiting to be claimed.

$6 billion of this is sitting in accounts with out of date personal details.

The remaining $8 billion in lost super is sitting in forgotten accounts that haven’t received a contribution in five years or more.