Lesson 2: Investing/Growing Our Wealth

Learning Objective

Identify appropriate investment opportunities to create wealth and develop an action plan.

We have three major resources that are vital in life, our wealth and our own personal development: money, energy and time.

Any investment that we make personally will require one or all of these resources. If we invest them properly, we create wealth. If we invest them poorly, we’re likely to end up with liabilities that reduce our resources.

If invested well, our time, energy and money can provide more opportunities for growth.

Unlike time and energy – money has no upper limit – energy and time are finite and can only be controlled to a point – money has infinite potential.

It’s often said that the best investment we can make is in ourselves; this provides us with the greatest return. This return may be financial but it may also be in greater knowledge, health, friendship, healthy relationships or personal growth.

While you might be surprised that the best investment is often in ourselves, when we develop ourselves to our full potential, create self-awareness, expand our knowledge, grow, and gain confidence then we increase our self-value, our mindset and our capacity to earn an income. And this can lead to new careers, passions and side jobs, better relationships, more fulfilment and more happiness.

Another great investment is in our professional and personal relationships and, of course, our children. The time, effort, love and reward of raising children is a significant investment, so too is the amount of money required.

# Truth The University of Canberra and AMP have identified that the cost of raising two children in Australia today is around $812,000 and rising. In fact, it’s more than double what it cost in 2002.

Financial investments

Have you ever heard someone talking about shares, stocks, bonds, or managed funds and were a little confused? Does the mention of investments or financial terms seem like a foreign language and a little overwhelming? Understanding some basic information about financial investments can be a great first step in learning not only how to invest safely and maximize the return on your money.

A financial investment is an asset that you put money into with the hope that it will grow or appreciate into a larger amount of money. This could happen if you decide to sell it later at a higher price or earn money on it while you own it.

A financial investment could be something that you’re looking to grow over the next year or two or even the next thirty years.

How much time you have on your side when it comes to your investment is often a key thing to consider when deciding what to invest in. Generally speaking, the more time you have, the more risk you can usually take. The more risk you take, the more potential for making more money.

You can choose to invest your money in a range of investments to help spread the risk and to match your goals and investment time frame. Typically speaking, cash and fixed interest are more suited to those people with a shorter time frame for investing, or a lower tolerance to risk. Property and shares offer the chance for higher returns at a higher risk and will typically need a longer time frame for investment.

It’s important that you get the mix of investments right to balance risk versus return on offer.

Mindful reflection/questions: What has been your best non-financial investment?

What has been your best financial investment?

What has been your worst investment?

On reflection, how could have this have been a better investment; what could you have done differently?

managing Risk

Financial risk is when an investment may or may not give us the outcome we want. For example, we expect our investment to grow but instead it falls in value, or we expect to earn regular interest of 6% but interest payments fall to 4%. Or, we expect to be able to access our money whenever we need but we aren’t able to access it.

In financial speak, the risk associated with a financial investment is often referred to as the volatility of the investment. The more volatile an investment, the higher the fluctuations you can expect in the return you receive from that investment.

Mindful Exercise:

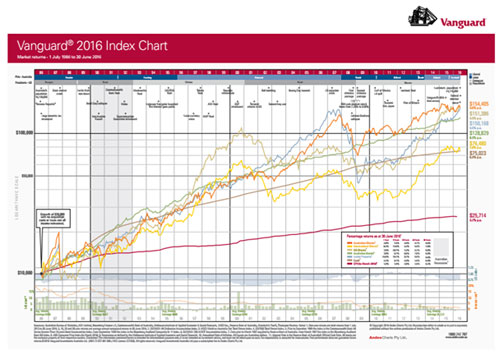

Have a look at this chart: https://static.vgcontent.info/crp/intl/auw/docs/resources/index_chart.pdf

This chart shows the growth of $10,000 since 1985. You’ll notice there’s a lot going on, but I’d like you to just focus on two things:

The brown line which represents cash investment.

The orange line which represents investment in Australian Shares.

Imagine investing shares is something new, something we’re uncomfortable doing so we decide to leave our money in cash for 30 years (the brown line).

30 years later our $10,000 would have grown to $86,815.

Now, imagine a different approach, we step outside of our comfort zone and put the same amount in Australian shares (the orange line) instead. While the returns will have fluctuated (gone up and down) more over the years, if we had actually remained invested for the full 30 years we’d have benefited significantly.

In fact, 30 years later our $10,000 would have grown to $215,685.

So that means the opportunity cost of playing it safe – choosing cash instead of shares – cost us $128,870 – our sometimes-safe option can be doing us more harm than good.

But stepping outside of our comfort zone can often involve us taking some kind of risk and being willing to take a risk doesn’t mean that everything will always work out. The key is to be able to weigh up the risk against the potential reward.

Reducing risk is all about managing risk.

One of the best ways to manage risk is to diversify.

Diversification is when we spread our money between different investments and asset classes such as cash, fixed interest, property and shares. This reduces the chance of being exposed to a single economic event, or risk in one asset class. If something we’ve invested in fails or does badly, we won’t lose all our money.

It’s the simple concept of not putting all your eggs in the one basket.

The power of compounding

When it comes to investing, you may have heard of the term compounding before. If not, it’s like the secret sauce to investing. It simply means the ability to earn money on your money, or interest on your interest.

Mindful Reading: this is a famous old tale

Once there was an Indian rajah who was impressed with the work of one of his servants, so impressed in fact that he decided to offer a reward for his dedication and hard work. When asked what he wanted for his reward, the servant courtier produced a chess board. He asked that one grain of rice be placed on the first square and doubled in each square after until all 64 squares were covered. The Indian Rajah thought it was an odd request, but he eagerly agreed. To his horror realised that because of the way that compounding works, that all the rice in the whole of India would not be able to cover the 64th square! In a rage at being deceived he ordered the beheading of his servant.

In this story, just one grain of rice in the first square seems so little. Even after 7,10,15 squares, the amount is still minimal. Yet time is a very important element when it comes to how compounding works.

How do we know what’s makes a good investment?

When investing we need to consider the return on our investment. To help us work out whether the returns offered by the investment opportunity are reasonable we should look at the expected returns for other similar things. If the returns seem very high in comparison, it can pay to be wary. When it comes to investing, the general principal is, the lower the risk, the lower the likely rate of return. Higher potential returns usually come with higher risks. Generally, we’ll need to take some level of investment risk in order to generate a reasonable return over time but it’s important to understand the risks and then keep within a level that we are comfortable with.

The Golden rules of investing

When it comes to making any investment, there are three simple, golden rules:

If it sounds too good to be true, it probably is

If you don’t understand it, don’t invest in it

Don’t rush an investment decision.

In fact when it comes to investing and financial matters don’t be fooled by fancy terminology, mind blowing statistics and slick presentations. Particularly if it all sounds too good to be true. It pays to do your own research, seek professional advice before making up your own mind.