Lesson 1: Earning, Spending and Saving

Learning Objective:

Understand the building blocks of our wealth practice are in how we earn, spend and save our money.

These principles create the foundation on which our journey to abundance is based and if we can learn to master these elements first then we will be well set up for our journey to abundance.

Put simply, when it comes to earning, spending and saving:

Earning is our ability to generate or make money.

Spending is how we manage our expenses, and

Saving is our ability to create a surplus.

Earning: money comes into our lives in many ways. Whether it’s our salary, a side job, investment income,

a gift, inheritance or winnings.

Spending: we spend money on needs and wants, emotionally and impulsively even without awareness. If we can create a better connection with our spending and understand our emotions that underpin our spending decisions, we can learn to control and plan our spending so that it is conscious and intentional. The money we have as a resource to use in our life is limited, so rather than wondering where it went at the end of each month, we need to be consciously telling it where to go. In other words, we need a spending plan. This means that we choose how, when and where we are allocating it. And this purposeful action can help us move closer to our goals.

Saving: saving isn’t something that comes naturally to all of us. Many of us have a why save when I can spend today kind of attitude. Instead of thinking about saving as something we have to do, why not think of it as a way to create opportunities and flexibility for the future.

The flow of money; earning, spending and saving

If we spend less than we earn, we have surplus money and can use this to reduce debt and build wealth. Most of us are good at one or two of these things, but many of us aren’t good at all three of them.

There is one simple equation that is fundamental to creating wealth:

Wealth = what we earn – what we spend.

Earning

Most of us tend to focus just on our ability to earn an income, yet we receive money in many different ways.

Creating a more conscious relationship with money requires you to become mindful, aware and grateful for the flow of money as it flows in and out of your life.

While money may be a finite resource in your life, it may be flowing to you in more abundance than you realise.

Money comes to us in the form of a gift, as income, interest on savings and investments, from the government, or even finding money on the road.

If you own a business or have a side business, you could even think of all the ways that customers/clients find you.

Mindful Exercise: Make a list of all the ways that money enters your life.

Mindful Question/Reflection:

Are there any other ways that you could attract more money into your life?

Could you ask for a pay rise?

Could you create a side job or make an income from a hobby?

Could you sell unused or unwanted possessions?

Could you earn more interest on your savings or a better return on your investments?

One of the quickest ways to open your life to abundance is gratitude.

Gratitude attracts more good things to be grateful for.

“Be thankful for what you have; you’ll end up having more. If you concentrate on what you don’t have, you will never, ever have enough.”

– Oprah Winfrey

When you cultivate gratitude, and be grateful for what you already have, you will naturally attract more for which you can be grateful.

Our definition of wealth is “when you have an abundance of anything in your life that you truly value”. This means wealth could be something material, a resource, an experience, a person or even a feeling. What you may not know is that you personally get to define what it is that makes you wealthy and you can work towards creating or having more of those things.

Once you know this, you discover that becoming wealthy and having abundance is actually easier than you think!

Mindful Exercise: Make a list of all the things wealth means to you.

This is all about getting clear on what’s important and what brings you true joy in life.

Don’t be afraid to list as little or as many things as you feel important in your life and which add to your feelings of wealth!

Optional Activity: Take two minutes each morning to write a gratitude list; celebrate abundance. We like this app: 21 Day Gratitude Challenge – you might like to try it too.

Time is Money; Money is Time

You may have heard the saying time is money. Have you wondered what that means?

We know that money is used as an exchange of energy. We exchange money for our time, knowledge, skills and experience. But do you know how much your real hourly wage is? The real hourly wage creates a connection between our time and our money. Knowing just how much an hour of our work time equates to us in cash (in our hands) can have many benefits.

Mindful Exercise: Calculating your real hourly wage is simple, start with your “real income”.

Your real income is your annual (gross) income minus any taxes and work related expenses.

Divide your real income by your total hours spent on work related tasks including the time it takes you to get to work, the additional hours or overtime etc.

Compare your real hourly wage to your paid wage.

*Note if you receive other “income” from Government support or investment income, add this to your annual income.

This gives you insight into how much you are actually earning or trading for your time.

Understanding what your “real income” actually is can have a very profound impact on your attitude to spending and saving as it creates a benchmark for your decision-making. It provides a true cost of an item in relation to how much time you are trading for it.

For example, let’s say your real hourly wage is $25 an hour after tax and work-related time and expenses. You see a pair of gorgeous shows on sale for $120. You can then weigh up whether working 4.8 hours is worth purchasing them.

Increasing our Income

Our ability to make money can be either passive or active.

Here are our top three tips for increasing our earnings:

- Educate ourselves: it’s often said the better our education the better our income. We might be able to get a new or better job or ask for a raise. Talking about raises, it’s important for us to be confident in our ability to negotiate a pay rise.

- Invest in things that generate an income. Rather than purchasing things that don’t.

- Sell stuff. We have a tendency to accumulate more and more stuff. In fact, we often rent storage sheds to house the stuff that we accumulate but which no longer fits into our homes. By decluttering we can reduce our stuff and free up cash by selling our unused or unwanted items.

Spending

Spending is actually a discipline and one that requires a lot of self-control. To get ahead we need to create a positive gap between our earning and our spending. We still want to enjoy life and we don’t want to become too frugal, but we need to find balance between living the good life and doing without.

Most of our spending typically falls into four categories:

- Emotional Spending: spending money to avoid negative emotions such as fear, pain, doubt, worry, or to make us feel happier. Sometimes this is due to a belief that we need to spend money to fix something or that by purchasing things we will be happier.

- Automatic Spending: a lot of our spending falls into this category: rent, mortgage, food, fuel. You don’t really think twice about spending money on these things as they’re often needs rather than wants. You don’t need to eliminate this type of spending but you do need to create consciousness around it.

- Impulsive spending: spending money on something that wasn’t a priority until we saw it. Ways to combat impulse spending is to shop only with a list, take cash only and remembering that we don’t have to buy things at that very point of time, we can always go back and get it.

- Occasional spending: outside of the usual budgeted items. It might be things like clothes, furniture, a new car, and a holiday.

- Planning our purchases.

- Shopping with intention and not just for something to do.

- Taking a list and sticking to it.

- Unsubscribing to the constant sales emails and offers.

- Asking questions like do I really need this before buying.

- Waiting before we buy something.

- Not buying something if we’re not 100% sure we need or want it.

- Choosing our shopping buddies wisely.

- Remembering our goals and weighing up if a purchase will get us closer or further away.

- Family and friends

- Cultural/Religious

- Ethical/ Emotional

- Social Media & Marketing

- Borrowing it

- Shopping around for it

- Making it

- Renting or hiring it

- Trading for it

- Buying a second hand version of it

- Automate it – we don’t miss what we don’t have. If we automatically put money into savings, before we get a chance to spend any of it, we’re more likely to do it!

- Create a reason for saving: just because or for a rainy day aren’t good enough and are likely to lose the argument when it comes to whether to spend or save. Save for an event, or a purpose or for a feeling. Make it personal.

- Make it little and make it regular: It’s better to save smaller amounts more often than it is to save big amounts on an adhoc basis.

We can create conscious, positive spending habits by:

Exercise – Download our “Should I Buy This?” Decision Tree. A Mindful Spending Decision guide to help you make more conscious spending decisions.

Whether we do so consciously or sub-consciously we apply our values to the way we spend money without really thinking about it. When it comes to our spending we often make choices according to our values that we may not be aware of. Shopping for local, organic, fair trade, eco, sustainable, cruelty free, recycled and second hand items are often indicators of our value system.

Many factors influence our decision to spend money or consume products.

These influences can include:

Regardless of what we earn, most of us spend right up to our earnings, irrespective of what they are. When we get a payrise: something is triggered in our sub-conscious and we lift our spending to use up that pay rise – we don’t even know we are doing it.

If we learn to be mindful of our money, influences, wants and needs we can shift our focus and create a life of abundance.

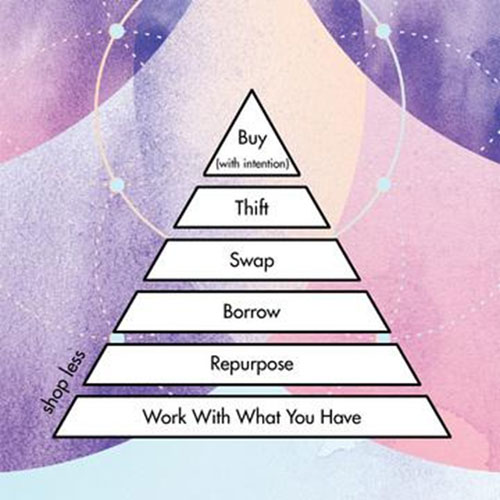

Spending Alternatives

In some cases, there may be alternatives to us actually buying an item. While it might seem obvious, often we forget about the alternatives we have to buying brand-new.

Instead we could consider:

Mindful Question/ Reflection

Think of the most recent item you purchased for your home. Perhaps it was a new kettle, a bath mat, or a new kitchen bowl. Ask yourself:

Could I make this?

Could I borrow this?

Could I buy this cheaper or second hand?

Could I substitute this with something else?

Could I get this somewhere else cheaper?

These questions help create awareness and open us to the option of considering alternatives to the way we currently spend or use our money.

Affirmation: I am open to alternatives.

Saving

Saving is a habit and something that we can learn to do with a little discipline.

Here are 3 tips to build a savings habit:

Spend less or Earn More

When it comes to increasing our savings, should we spend less or earn more? There are arguments for both. Spending less is probably the easiest and quickest way to see the biggest changes in our ability to save, but the problem with cutting our spending is that it can only go so far before it is no longer fun or viable.

Instead we could look at ways to increase our money. The best part about earning more is that there isn’t actually a limit to what we can earn. The most common way to earn is through a job, but we could look at other creative ways to make some more cash on the side.

Often it’s more important to have balance – a little more income and a little less spending can work wonders for us.

It’s not how much money you have; it’s what you keep that matters!

Mindful Question / Reflection:

What has been your biggest purchase in the last 30 days?

Where have you spent your money most frequently?

Have you had to pay any late fees?

How much of your spending was on stuff that you needed?

How much was on stuff that you wanted?

Did you pay ATM fees for using another bank’s ATM?

Up for a Challenge?

Why not try a no-spend week or fortnight? If you’re feeling brave even a month.