Lesson 5: Planning for the Future

Learning Objective

Connect with the future version of yourself and take action to turn knowing into doing.

Studies on the brain actually show that we tend to think of our future selves as strangers and someone we don’t really know. Because of this we find it hard to imagine and connect with the future version of our self, which means we tend to prioritise our current self (now) over our future self (later).

Mindful Exercise: Try connecting to your future self

Think ahead to 10 years time.

Think about the life you want to be living.

Where are you?

How will you be spending your time?

Who will you be spending it with?

Who have you become?

What about in 10, 20 years, 30 years

Mindful Question/Reflection

What did your future look like?

Did you have any procrastinating thoughts?

Procrastination: put simply means we put something off until later, or defer it.

It’s okay to procrastinate with some things, but if we’re procrastinating with a task that is both important and urgent – then it can become a problem.

We all procrastinate more than we’d like. So what if we stopped? Could we really accomplish more? On average we spend 2 hours a day procrastinating. Use this clever procrastination calculator to work out exactly how much time you’ve spent procrastinating and what you may have been able to otherwise accomplish in that time instead.

The most common reasons we procrastinate with our money are:

- We find it boring or there are other things we’d rather be doing.

- We don’t know how to do it so we avoid it.

- We are perfectionists and we don’t have the time to do the task perfectly.

- We don’t know where to start.

- We don’t think there is sufficient benefit in us doing it.

While it’s human nature to procrastinate when it comes to our money, our procrastinating habits may eventually create a problem or we might end up regretting not taking action sooner.

Here are some simple ways we can stop procrastinating:

- Do the task first, and then reward yourself by doing something you love.

- Break it down into smaller tasks, do little bits more frequently.

- Write it down – a to do list helps create a checklist for you to monitor your progress and helps create momentum.

- Enlist someone else to do it with you, or to help you.

- Consider the pain and consequence of not doing it by asking yourself “will this really be better if I put it off?”

- Focus on the good feelings (satisfaction/achievement/joy) you’ll have when it’s done.

Learn how procrastination affects our financial futures and what we can do to fight it.

Mindful Exercise: Your Procrastinator personality is revealed here:

Remember, we are all motivated by different things so what works for one will be different to what works for another.

Turning Knowing into Doing

Knowing something and actually doing it are two different things.

We know we should stop procrastinating, we should save more money, watch less television or buy less take away coffees. But knowing something is one thing. Actually doing it is another and it’s the doing part that is the hardest.

It’s often referred to as the Knowing-Doing Gap.

Here are the top reasons why we don’t do the things that we know we should and how to tackle them:

Knowing: we don’t know how.

Doing: get educated about your money.

Knowing: we’re afraid of being different, of failure, of change and fear stops us.

Doing: overcome fear by facing it or you can get help to tackle it.

Knowing: we’re just not motivated enough.

Doing: make the reward more worthwhile.

Knowing: we equate talking about something as doing it.

Doing: we need to actually implement the decision when it’s made.

Now vs. Future

If we’re too focussed on the present, then we may not have much of a future, but if we’re too focussed on the future, we may miss all the great things that are happening today. Like all things, the key is balance.

The key is balancing living in the now with planning for the future.

Most of us understand, at some level, the need to save for our long-term goals. Buying a house, preparing for retirement, or paying for children’s schooling are goals that we may have to save for.

But why is it that we often fail to put aside the money needed? Perhaps we don’t understand how much difference it can make if we start now versus later?

I’ll do it later, sound familiar? It might not be your fault. Studies show our brains get fatigued from all the little decisions we make every day. So what happens if we take a break? Could procrastination actually make us more productive?

Many of us put off saving, paying down debt or putting in place a plan for our wealth creation thinking we’ll be fine if we start tomorrow, or next month, perhaps even next year? We might feel like we can’t afford to save or make higher repayments on our debt now, but in reality we can’t afford not to!

We might tell ourselves that our living costs today make it too difficult to start saving for tomorrow. We’ll convince ourselves it’ll be easier to begin to save for the future when we get a pay rise. The reality is though that the longer we put it off, the harder it will be for us to achieve.

There is actually a cost of waiting.

But what do these two things actually have to do with one another?

Let’s Begin…

Saving now vs. later

Meet Annabel, she is 25. She starts investing $100 a month for 10 years.

By the age of 35, she’s saved $12,000 and assuming she receives a return of 6% her balance would be $15,996.

She then stops investing and leaves her money in an account that continues to grow at 6% pa. By age 65, the account is valued at $91,873.

Now, meet Alicia.

Alicia isn’t quite ready to invest in her 20s and decides to defer until she turns 35. At 35, Alicia begins with $100 a month, for 10 years. At age 45 she stops.

Over that time, Alicia would have contributed $12,000 and assuming she receives a return of 6% her balance would be $15,996.

Alicia leaves her money until age 65 too.

But at 65 her account balance is only $51,301.

That’s a $40,572 difference!

What about debts?

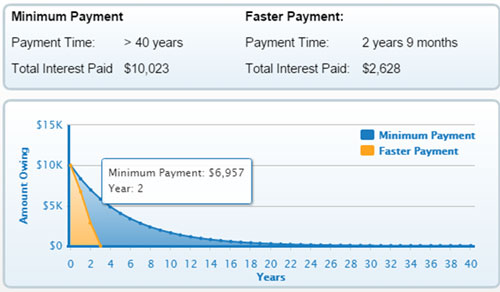

The same scenario could be used to show the impact of compounding has on debt, and the benefits of paying down debt sooner. Let’s imagine for a moment that both Annabel and Alicia have $10,000 in credit card debt.

The both pay the minimum balance each month and pay interest of 18% on their balance.

Annabel decides to pay an extra $100 per month off the balance.

Alicia decides not to.

The difference may surprise you.

For Alicia, as she’s only making the minimum repayments, it will take her 40+ years to pay off the credit card balance at this rate. In total she’ll pay $10,023 in interest over that time.

But for Annabel who makes an extra repayment of $100 a month, she’ll have her card paid off in just 2 years, 9 months. And the amount of interest she’ll pay reduces to $2,628!

Pretty crazy, right?

Congratulations! You’ve reached the end of Module 3

Well done on completing the first half of your journey. Keep an eye on your inbox, and we’ll send you an email when Module 4 is available (you’ll get one

module each week). Until then, we’d love to hear your feedback or help you

with any questions you may have.

Best wishes,

Lea + the mindful wealth movement team.

Feedback

What is one insight or key reflection that you have taken away from this module?

What is one action your going to take with your wellth (wealth & wellbeing)?

Did you enjoy and get value out of the content in module 3?

We really value your feedback and suggestions for improvement – please share how you think we might be able to improve…