Lesson 3: The Places/People to find advice

Learning Objective

Knowing when to seek advice and where to get it from

There are many places we can choose to get advice from when it comes to managing our money. Typically, we’ll seek advice from; partners and family; banks and financial advisors; social networks and community groups; media and of course, friends.

But what makes a reliable source of information?

We live in an age of information overload. Being able to distinguish what is useful advice and what is not is a very important skill when it comes to our money.

Having the ability to access information and do research on any topic at the touch of a button can be extremely useful as well as dangerous when it comes to sourcing reliable information. We need to be able to distinguish between what is opinion and what is fact and whether the information is coming from a source that has a vested commercial interest or is independent advice. The internet and social media aren’t the only places where we may find questionable financial advice. Many of us have friends or family who feel compelled to give their heartfelt opinions on investment ideas and the media often has a habit of using emotive language to try and influence us

When it comes to our finances, we should remember that they’re extremely personal and what is right for one person may not be right for us as we may have a completely different set of circumstances. While it is great to be able to take in a range of information from various sources, it’s best to seek professional advice when it comes to important life decisions, transitions or even our own goals and plans with money.

There can be a lot of bad press around the financial planning industry and rightly so in some cases. But often it’s more of a case that a few bad ones spoil it for all the rest. The industry as a whole has been changing for some time, for the better mostly and it’s becoming a lot more transparent so that we can decide whom to trust and whom not to trust.

There is a big misconception in society that to see a financial planner or coach, we need to be wealthy. But this is not the case.

A man (or woman) is not a financial plan

Most of us don’t like to admit it, but many of us have been there: secretly hoping that someone or something will appear and solve all our money problems. It’s not really our fault, from a very young age we were raised with stories of fairy tale princesses who had princes on white horses ride up and save the day. We’ve come from a culture where traditionally men were the bread winners and women were the nurturers and housekeepers. It’s no surprise that many of today’s modern women have a rescue complex… a mentality that a partner, the lottery or an inheritance will save them financially.

This type of mentality can be very detrimental to our finances. We need to take responsibility for our own financial future and well-being and take steps (action) towards creating the future that we want, or making the changes needed in order to start living the life that we want. We can’t sit back any longer and hope and dream that things will change!

We all use money and we could all benefit from having a coach and trusted adviser to help us manage our money a little better.

Just like we’d seek a teacher or coach if we wanted to get better at a particular sport or hobby, learning to manage money is a skill and one that we can master quicker and easier if we have someone to help us and keep us accountable.

Taking the first step in selecting a financial adviser or coach can be daunting. After all, we’re selecting someone to help us achieve our goals, manage our money, give advice – it’s a big decision and we need to trust them.

To simplify the process, first figure out where you are in your life and what services you need. Specifically, consider whether you need help saving money or getting out of debt, growing existing savings, or a more comprehensive view of your finances across many different areas.

While traditionally you may go to a financial coach to help you save money or work on your money mindset, a financial advisor or planner to help you grow, protect or invest that money, these days the the lines between coach and planner are blurring.

As you research financial service professionals, be sure to look at their qualifications, such as educational background, relevant work experience, and certifications, to get a better understanding of what makes a particular person right for you. Be sure to understand their areas of expertise and limitations, as well as how they are remunerated.

Mindful Exercise: Get to know what financial planners and advisors really do.. The most common misconception about financial planning and advice is that it’s all about investment management; that financial advisers exist just to tell you how to invest your savings. While that is part of what they do, it’s not the whole picture.

Download our Financial Planning Explained guide to explore what a good financial planner / advisor can help you with.

Mindful question/reflection: Of course, making sure financial advisors are accredited and have sufficient training, experience and knowledge is very important. To consider how compatible they are for you, ask the following questions:

Do they know my situation?

Are they an expert in their area? Or have they had experience in a similar situation?

Is there a cost for their advice?

Will they benefit in any way from us taking their advice?

Is it in our interest or their interest that they give us advice?

If professional, are they employed by or aligned with a company that will bias their advice or restrict them?

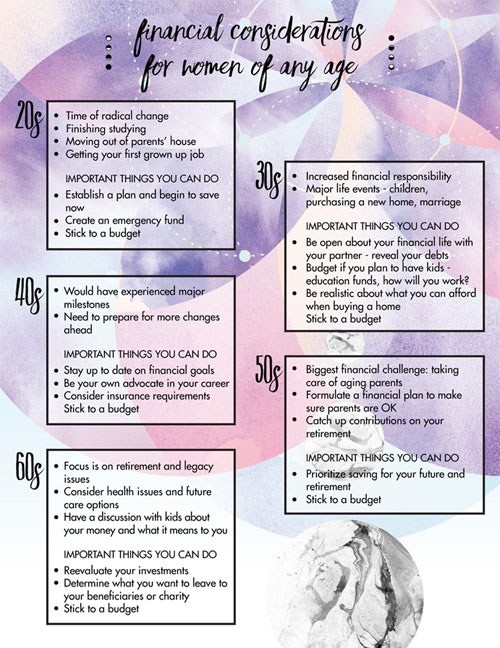

Life Events we face as women

Women in their twenties, thirties, forties, fifties and sixties all face decade-specific challenges and opportunities in order to create financial well being for themselves and their families.

We have a number of events in our lifetime include: marriage, divorce, travel, having children, educating children, starting a business, bankruptcy, facing Illness, redundancy, moving, renovating, studying, changing careers, becoming a caregiver, becoming a grandparent, losing a partner – the list goes on!

So how do we manage these life events and how do we know what we should be focussing on as we get older? While everyone is different and has a unique life path, there are some common themes that we can focus on through our 20’s to our 60’s and beyond.

A plan makes things happen. To achieve a goal you must plan how to make it happen. A goal without a plan remains just a goal – many people have ideas and dreams, which are never realised, because they’re not planned.

You cannot ‘do’ a goal but you can do the things that enable it to be achieved – usually several through a succession of several steps.

A good plan identifies causes and effects in achievable stages.

Even the most ambitious goals and plans are achievable when broken down and given a realistic time-frame, appropriate effort and focus.